Planning for retirement is one of the most important financial decisions anyone can make, and in the United Kingdom, understanding the concept of pensionable age is central to that process. Pensionable age refers to the age at which an individual becomes eligible to receive their State Pension. While it may sound straightforward, the rules surrounding it have evolved significantly over time, reflecting changes in life expectancy, economic conditions, and government policies.

For many people, retirement is no longer seen as a fixed milestone but rather a flexible phase of life. This shift makes it even more important to understand how pensionable age works, what factors influence it, and how it impacts long-term financial planning. Whether you are just starting your career or approaching retirement, having clarity about these aspects can help you make informed decisions and secure your financial future.

The Evolution of Pensionable Age in the UK

The concept of pensionable age in the UK has undergone several changes over the decades. Historically, the State Pension age was set at 65 for men and 60 for women. However, with increasing life expectancy and the growing financial burden on public funds, the government introduced reforms to equalize and gradually increase the pension age.

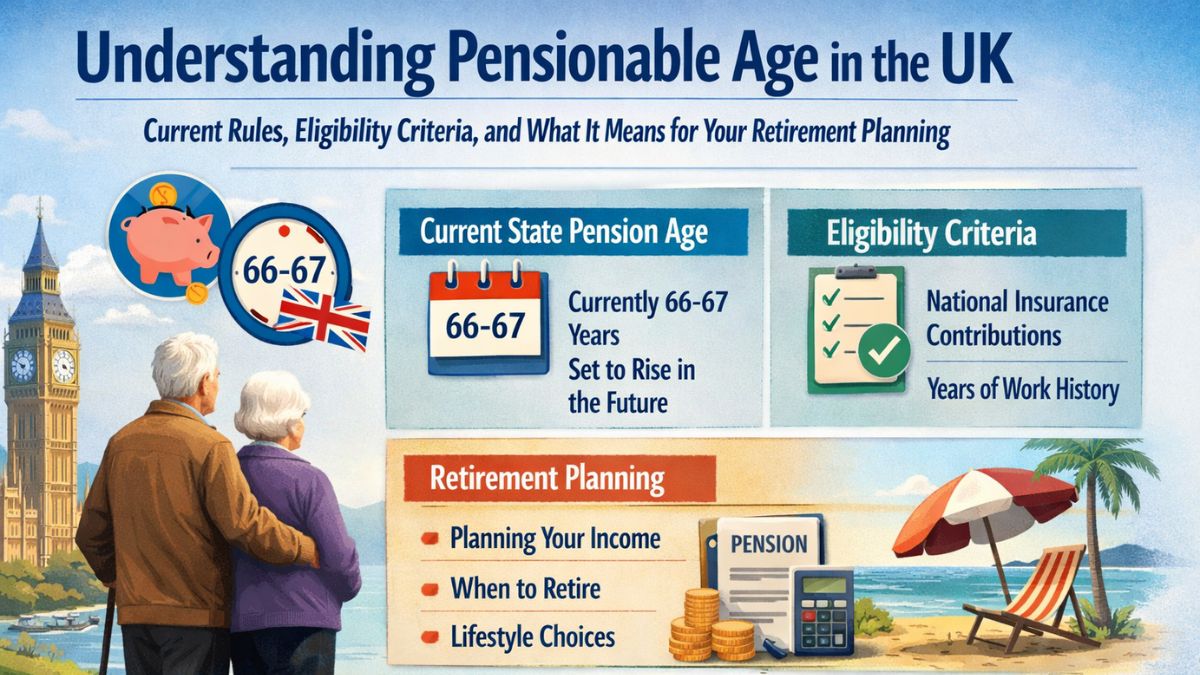

Today, the State Pension age for both men and women is rising, and it is currently set at 66. Further increases are already planned, with the age expected to rise to 67 and eventually 68 in the coming years. These changes are part of a long-term strategy to ensure the sustainability of the pension system while encouraging people to remain in the workforce for longer.

The gradual increase in pensionable age has sparked discussions and debates across the country. While some see it as a necessary adjustment to modern realities, others express concerns about its impact on those in physically demanding jobs or with limited savings. Regardless of these differing perspectives, the changes highlight the importance of staying informed and adapting retirement plans accordingly.

Current Rules Governing Pensionable Age

The current rules surrounding pensionable age in the UK are primarily determined by legislation and government policy. The State Pension age applies to everyone, but the exact age at which you can claim your pension depends on your date of birth. This means that individuals born in different years may have different pensionable ages.

In addition to age requirements, eligibility for the State Pension is also based on National Insurance contributions. To qualify for the full State Pension, individuals typically need at least 35 qualifying years of contributions. Those with fewer years may still receive a partial pension, depending on their contribution history.

It is also important to note that reaching pensionable age does not automatically mean you must stop working. Many people choose to continue working beyond this age, either for financial reasons or personal fulfillment. In such cases, individuals can choose to defer their State Pension, which may result in higher payments later on.

Eligibility Criteria and Key Requirements

Eligibility for the State Pension involves more than just reaching a certain age. One of the most critical factors is your National Insurance record. Contributions are usually made through employment, self-employment, or voluntary payments. These contributions build up over time and determine the amount of pension you are entitled to receive.

For individuals who have gaps in their contribution record, there may be opportunities to fill those gaps by making voluntary contributions. This can be particularly beneficial for those who have spent time out of the workforce due to caregiving responsibilities, education, or other reasons.

Another important aspect of eligibility is residency. Generally, you must have lived or worked in the UK for a certain period to qualify for the State Pension. However, international agreements may allow individuals who have worked in multiple countries to combine their contribution records, depending on the specific arrangements in place.

Understanding these criteria is essential for effective retirement planning. By reviewing your National Insurance record and identifying any gaps early on, you can take proactive steps to maximize your pension entitlement.

The Impact of Pensionable Age on Retirement Planning

Pensionable age plays a crucial role in shaping your overall retirement strategy. It determines when you can start receiving your State Pension, which is often a key component of retirement income. However, relying solely on the State Pension may not be sufficient to maintain your desired lifestyle, making additional savings and investments essential.

One of the key challenges in retirement planning is aligning your financial resources with your expected retirement timeline. As pensionable age increases, individuals may need to work longer or rely on other sources of income to bridge the gap. This could include workplace pensions, personal savings, or investments.

The uncertainty surrounding future changes to pensionable age also underscores the importance of flexibility in your retirement plan. By building a diversified portfolio of income sources, you can reduce your dependence on any single factor and better adapt to changes in policy or personal circumstances.

Workplace and Private Pensions: Complementing the State Pension

While the State Pension provides a foundation, it is often supplemented by workplace and private pensions. Many employers in the UK offer pension schemes that allow employees to contribute a portion of their salary, often matched by employer contributions. These schemes can significantly enhance your retirement income over time.

Private pensions, on the other hand, offer individuals the flexibility to save independently. These plans can be tailored to suit individual financial goals and risk tolerance, providing an additional layer of security for retirement.

The combination of State, workplace, and private pensions creates a more robust financial framework. By contributing regularly and taking advantage of compound growth, individuals can build a substantial retirement fund that supports their long-term needs.

Challenges and Considerations for Future Retirees

As the pensionable age continues to rise, future retirees may face a range of challenges. One of the most significant concerns is the ability to work longer, particularly for those in physically demanding professions. Health issues, job availability, and economic conditions can all influence an individual’s ability to remain in the workforce.

Another challenge is the increasing cost of living, which can erode the value of pension income over time. Inflation, housing costs, and healthcare expenses are key factors that need to be considered when planning for retirement.

Additionally, changes in government policy can create uncertainty. While reforms are often introduced to ensure the sustainability of the pension system, they can also impact individual plans. Staying informed about policy changes and regularly reviewing your financial strategy can help mitigate these risks.

Preparing for a Secure Retirement

Preparing for retirement requires a proactive and informed approach. Understanding pensionable age is just one piece of the puzzle, but it is a crucial starting point. By gaining a clear understanding of the rules and eligibility criteria, you can make better decisions about when and how to retire.

Regularly reviewing your financial situation, setting realistic goals, and seeking professional advice can all contribute to a more secure retirement. It is also important to consider non-financial aspects, such as health, lifestyle, and personal aspirations, when planning for this stage of life.

Building a strong financial foundation early on can provide greater flexibility and peace of mind in the future. Whether it involves increasing your savings, investing wisely, or exploring additional income streams, every step you take today can have a significant impact on your retirement outcomes.

Conclusion

Understanding pensionable age in the UK is essential for anyone looking to plan for retirement effectively. With evolving rules, changing eligibility criteria, and increasing life expectancy, the landscape of retirement planning is more complex than ever before.

However, with the right knowledge and preparation, it is possible to navigate these changes with confidence. By staying informed, taking proactive steps, and maintaining a flexible approach, you can build a retirement plan that meets your needs and supports your aspirations.

Ultimately, retirement is not just about reaching a certain age but about achieving financial security and enjoying the freedom to live life on your own terms. Understanding how pensionable age fits into this broader picture is a key step toward making that vision a reality.

FAQs

1. What is the current pensionable age in the UK?

The current State Pension age in the UK is 66 for both men and women, with plans to increase it further.

2. How many years of contributions are needed for a full State Pension?

You typically need at least 35 qualifying years of National Insurance contributions to receive the full State Pension.

3. Can I work after reaching the pensionable age?

Yes, you can continue working after reaching pensionable age and even delay your State Pension for higher future payments.